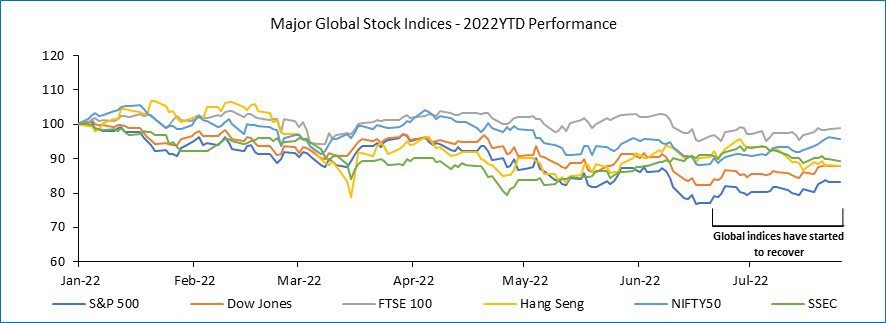

Markets had a bullish run in 1H2021 due to the reopening of economies from lockdowns and the arrival of Covid vaccines sparked a worldwide recovery for financial markets in late 2020. However, 2022 has been painful for investors with a majority of the global benchmarks giving negative YTD returns. The S&P 500 registered its worst first half (-20%) since 1970 and its 2nd worst 1H since its inception in 1957. The Dow Jones Industrial Average suffered its biggest half-year decline since 1962. Asian stock markets too plummeted and faced their worst 1H since 2008. The stocks struggled to rebound due to global recession worries and aggressive tightening by central banks triggering heavy outflows of funds from emerging markets.